A Munger PA Investment

Black Hills Corporation

Reading foundation filings is an interesting way to see what otherwise private people have invested in personally.

This is a neat trick for examining both Buffett's and Munger's PA investments. It's how I first learned about Hayes Lemmerz.

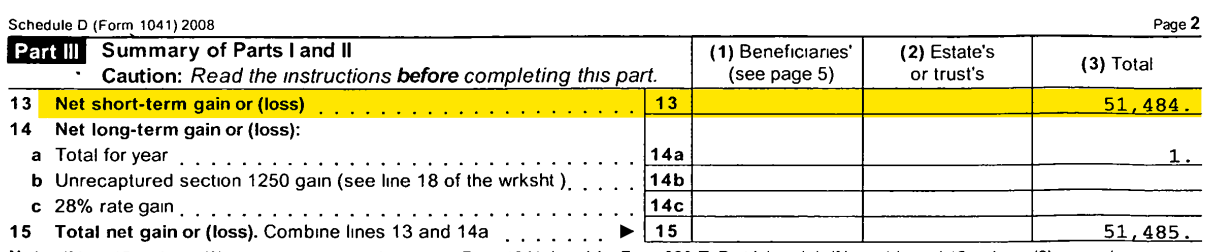

Form 990-PF is public record. It shows contributed and purchased securities, cost basis, sales proceeds, and a slew of other information.

The Alfred C. Munger Foundation (named for Charlie's father) sold 10,000 shares of Black Hills Corporation (BKH) for $23 each in June 2009, resulting in a short-term gain of 29%.

Here's the source document:

A reasonable assumption based on this filing is that Charlie purchased this specific lot of 10,000 shares for $18 apiece in early 2009 and sold in June 2009 around $23.

He could have been buying the stock before that and holding shares after.

The only thing we know with reasonable certainty is that Charlie thought Black Hills was a good buy in 2009 at $18 per share.

This case study will examine what BKH looked like when Charlie bought it and what the ultimate results were, both over short and longer time frames.

Historical Set Up

Black Hills is a utility company based in South Dakota.

It was formed in 1941 through a combination of several existing utility companies serving the Black Hills region. The earliest predecessor traces its roots back to 1883.

This is a sleepy ho-hum electric and gas utility company. It has slowly compounded for decades, adding connections and making the occasional tuck-in acquisition.

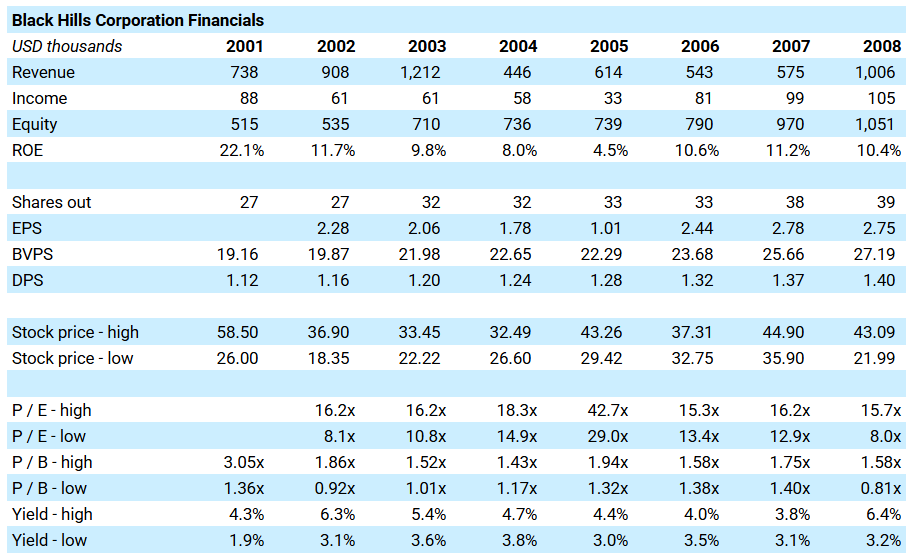

By 2008, BKH had shareholders' equity of just over $1 billion and served customers in four states (South Dakota, Wyoming, Colorado, and Montana).

Here's a financial snapshot from 2001 to 2008:

Black Hills could be described as a decent and predictable business in the years leading up to Charlie's purchase. ROE was in the low double digits and book value per share growth (adding back dividends) averaged 11% from 2002 to 2008.

Simple, clean, predictable, decent quality.

Valuation

Early 2009 was a great time to buy stocks. And BKH was no exception.

Black Hills earned $105 million in 2008 ($2.75 per share). It paid $1.40 of dividends that year and finished the year with $27.19 of per share book value.

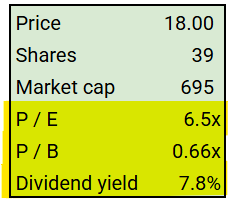

Here's the valuation Charlie's foundation paid for its shares in early 2009:

I think the thesis here was pretty simple.

A durable, safe business that earns double digits on equity shouldn't trade for 66% of book value.

The crashing economy wasn't going to kill the utility business. People still needed to turn their lights on and fire up the stove.

BKH was a relatively small $695 million market cap at Charlie's purchase price, which is probably why he bought it personally and not for Berkshire or Daily Journal.

Results

BKH's average price three years later in 2012 was $33.66 per share, good for a return of 98% (25% CAGR) before dividends.

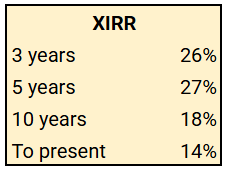

Here's the forward IRR (including dividends) for various timeframes after Charlie's purchase:

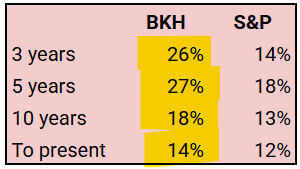

I asked ChatGPT to give me the S&P 500 total return over the same periods. Here's the comparison:

So, Charlie's pick handily outperformed the S&P over both short and medium timeframes. The long-term result is closer.

Black Hills has paid out $31 of dividends per share (172% of Charlie's $18 cost) and now trades for more than $70 per share.

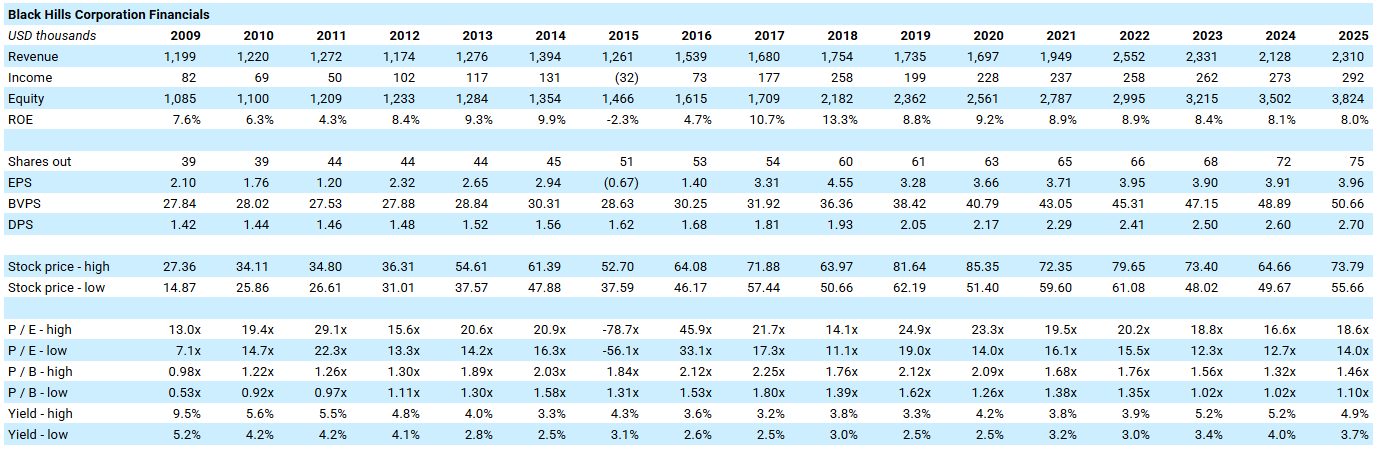

Here's the financial record since 2009:

Takeaways

The Black Hills case isn't terribly exciting, but I do find it interesting and useful.

If I had to nail it down to one simple idea it would be this:

Buying an adequately capitalized business, that should earn at least a high-single-digit return on its common equity, at a substantial discount to book value often works very well over short- and medium-term time frames.

The beauty of these sorts of investments is that the downside is protected by tangible equity, while the upside is driven by earnings and multiple re-rating. Low risk, high return.

This is value investing nirvana.

That said, as Charlie pointed out multiple times over the years, the longer you hold this sort of business, the closer your annual return trends towards the ROE.

You can't earn 20%+ per year for decades by sitting on something that earns 9% on equity. The benefit of multiple expansion gets diluted over time.

Still, BKH with its mediocre 8-11% ROE has delivered 14% per year from 2009 to present.

Good results can be achieved over long time frames (with low risk) by buying merely average businesses at cheap prices.

Disclaimer

This post was written by Joe Raymond, an investment advisor representative and agent of Caldwell Sutter Capital, Inc. (CSC). These contents reflect the opinions of Joe Raymond and not CSC. This content is for informational and entertainment purposes only. Nothing herein constitutes financial, investment, legal, or tax advice, nor should it be construed as a recommendation to buy, sell, or hold any securities or assets. Investing involves risk, including the loss of principal, and past performance does not guarantee future results. The information provided is based on publicly available data and personal opinions, which may not be complete, accurate, or up to date. Any investment decisions you make should be based on your own research and consultation with a qualified financial professional. The author(s) and publisher assume no responsibility or liability for any actions taken based on the content provided.